I pulled up a table to calculate the global tungsten mine production distribution in 2024, and the data is chillingly stark.

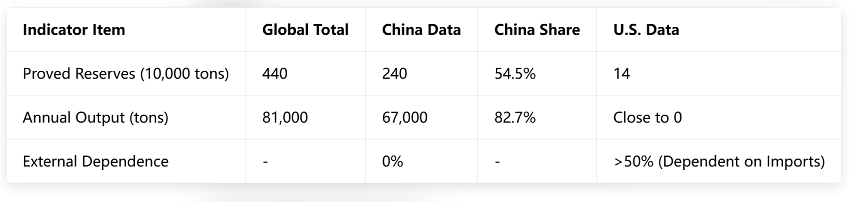

According to the latest statistics from the U.S. Geological Survey (USGS), global tungsten mine production in 2024 was approximately 81,000 tons. Of this, China produced 67,000 tons, accounting for a staggering 82.7%. Vietnam, Russia, and Bolivia, which followed, combined only accounted for a fraction of our output.

Many people don’t have a clear understanding of what “over 80% share” means. In high-end manufacturing, this isn’t just “leading,” it’s “absolute dominance.” Tungsten, nicknamed the “teeth of industry,” is considered by military experts to be an indispensable “metallic ration” in modern warfare.

I. A Resource Card That Determines War and Peace

We must understand that the current surge in tungsten prices is not merely speculation in the capital markets.

I compared the global tungsten mine production and reserves over the past 10 years. In 2014, China maintained a relatively relaxed export policy, and tungsten prices were incredibly low. However, by 2024-2026, with the normalization of protective mining of strategic resources and environmental inspections, the global supply and demand balance has been completely restructured.

Global Tungsten Mine Production and Reserves Comparison Table (2024-2025 Data)

This data illustrates an awkward fact: although the United States has certain reserves, due to environmental costs, labor costs, and a gap in beneficiation technology, they have not engaged in large-scale primary tungsten mining for decades.

This has created an extremely strange situation: as the Middle East’s powder keg smokes and the war of attrition in Eastern Europe intensifies, NATO countries find that the most crucial raw material for increasing armor-piercing projectile production is in the hands of what they consider their “main adversary.”

II. The Achilles’ Heel of Armor-Piercing Projectiles: Why Tungsten is Essential?

In tank battles, the decisive factor is often not whose armor is thicker, but whose projectile core is harder.

Currently, the mainstream long-rod discarding sabot armor-piercing projectiles (APFSDS) have only two core material options: depleted uranium or tungsten alloy. The United States, due to its nuclear waste disposal needs, previously used depleted uranium projectiles on a large scale. However, the radioactive contamination and logistical burdens of depleted uranium projectiles are immense, leading even the US military to accelerate its shift towards tungsten alloys.

I have studied the manufacturing process of tungsten alloy projectile cores. It’s not a simple melting process; rather, it involves mixing tungsten powder, nickel powder, and iron powder in specific proportions and sintering them using powder metallurgy.

There are two critical hurdles:

Raw material purity: Military-grade tungsten powder requires a purity of over 99.95%, with impurities controlled within the million-level.

Manufacturing process: Currently, only a very few countries globally, including China, Germany, the US, and Russia, truly master the deformation processing technology for this high-density alloy.

The current situation is that due to China tightening exports of primary tungsten products, the price of tungsten concentrate on the international market has surged in the short term. For Western military factories, this means they have to pay a “resource premium” several times higher than three years ago for every armor-piercing projectile they produce.

III. The “Heat Shield” for Aerospace and Hypersonic Weapons

If we shift our focus from the ground to the sky, the importance of tungsten becomes even more alarming.

When hypersonic missiles fly at speeds exceeding Mach 5, the surface temperature of the warhead can instantly soar to over 2000°C. In this extreme environment, most metals soften like butter.

Tungsten has a melting point of 3422°C, the highest of all metals. To address the issue of high-temperature resistance, the aerospace industry requires large quantities of tungsten-copper alloys or tungsten-infiltrated ceramic materials. I examined the global order flow for aerospace-grade tungsten materials in recent years and found that even amidst the West’s clamor for “decoupling,” major European aerospace companies are still frantically stockpiling high-purity tungsten targets and tungsten sheets produced in China through trilateral trade.

This dependence isn’t because they want to, but because only China’s supply chain can simultaneously provide both “high purity” and “large quantities.”

IV. The “Invisible Killer” in the Semiconductor Chain

Many people are unaware that tungsten is also an absolutely core material in semiconductor manufacturing.

In the chip wiring process, a key gas is needed: tungsten hexafluoride (WF6). It is used for chemical vapor deposition (CVD) to build tiny conductive channels between transistors.

I reviewed industry data from recent years. For a long time, the global WF6 market was dominated by Japan’s Kanto Denka and South Korea’s SK Materials. However, starting in 2022, Chinese companies began to emerge as strong competitors.

The underlying logic of this rise is very solid: Chinese companies directly have access to the world’s largest tungsten mines.

When international tungsten prices soared by 500%, Japanese and South Korean companies had to pay exorbitant logistics and premium costs to procure raw materials, while Chinese companies enjoyed “affordable raw materials” right on their doorstep. This is not only a game of resources, but also a game of cost pricing power.

Once Chinese companies achieve full domestic production of WF6 and other specialty gases, we will not only control the West’s armor-piercing projectiles, but also seize a vital lifeline in global semiconductor precision manufacturing.

V. The Vicious Cycle of Restarting Mines and the Growing Pains in the West

I compiled a table comparing mining and ore processing costs between China and the US. This difference isn’t just about labor costs; it represents a fundamental shift in the industrial ecosystem.

Global Tungsten Mining Cost Comparison (2025 Projection)

This means that if China doesn’t raise prices, the US will lose money on every mine it opens. If China raises prices, the US military’s procurement budget will explode.

Even more critically, mining is only the first step. Tungsten ore cannot be used directly after mining; it requires complex chemical processing to become ammonium paratungstate (APT). Currently, 90% of the world’s APT production capacity is in China. If the United States wants to bypass China, it not only needs to mine but also needs to build an extremely polluting and energy-intensive chemical smelting chain domestically.

Under their legal system, environmental impact assessment lawsuits just for tailings ponds could take ten years. During this time, the consumption of armor-piercing rounds on the front lines won’t wait for your report to be completed.

VI. Market Share Acquisition: The “Dimensional Reduction Attack” of Photovoltaic Tungsten Wire

Besides the military industry, China is leveraging the physical properties of tungsten to seize market share from Japanese and South Korean companies in high-end civilian sectors. The most typical example is photovoltaic fine tungsten wire.

Previously, carbon steel wire was used for cutting silicon wafers. To make silicon wafers thinner and reduce wear, the cutting wire had to become increasingly thinner. Carbon steel wire reaching 35 micrometers is almost the physical limit; any thinner and it breaks. This is where tungsten wire comes in.

Technological Dominance: Chinese companies have developed ultra-fine tungsten wires with diameters down to 28 micrometers or even finer.

This high-precision wire drawing market was originally monopolized by Japanese companies. However, Chinese companies, through the synergy of their entire industrial chain—”own mines + own smelting + own wire drawing”—quickly reduced costs to half that of Japanese companies.

As a result, while Japanese and German companies were still calculating costs in the lab, Chinese companies had already cleared out the photovoltaic cutting market. This scale effect, in turn, further reduced R&D costs and strengthened our technological lead in military-grade tungsten powder.

VII. How can resource dividends be translated into wages for ordinary people?

Many people think that rising mineral prices only benefit business owners and have nothing to do with ordinary people.

In the past, through fierce competition and price wars, we sold strategic resources at bargain prices, while miners received meager manual labor wages.

Now, through export quotas and industrial integration, the unit price of our tungsten products has increased, and profits remain domestically.

R&D Premium: Chinese engineers specializing in powder metallurgy and precision molds are beginning to earn salaries comparable to those in first-tier cities.

Industrial Clusters: A high-end tungsten processing base can drive tens of thousands of high-end supporting jobs in the surrounding area.

When China controls the pricing power of raw materials, we are no longer just “porters” at the bottom of the industrial chain, but “landlords” who collect taxes. This retention of profits is the foundation for supporting the Chinese engineering talent dividend and improving the living standards of ordinary people.

VIII. Strategic Resolve: Don’t fear price increases, fear shortages.

The current surge in tungsten prices is actually a belated “return to value.”

The West may try to find alternative mineral sources in Australia or Africa, but as long as our deep-processing technologies (such as nano-tungsten powder and special coatings) and cost advantages remain, they cannot escape the “Chinese tungsten cycle.”

Although China has the largest reserves of tungsten, it is only enough to mine for about 30-40 years. We have no reason to continue selling off the “military rations” of future generations at rock-bottom prices for a little foreign exchange. This game will continue for a long time, but the initiative has returned to our hands.

We must get used to this normalcy of being overwhelmed by both “resources” and “technology.” This is not just about the outcome of a single armor-piercing projectile, but also a milestone in China’s shift in the global industrial chain from “providing labor” to “setting the rules.”

Author: Ms. Cherry Zhao, Sales Manager of FOTMA ALLOY, over 20 years of experience in Non-ferrous industry.

Post time: Mar-26-2026